Some notes from our recent monthly reports and our weekly 3-county report

·

3-county report

o

There are fewer active listings of single family

homes in both Marin and San Francisco than there are homes that are “pending” (already in contract). Same situation last month. While this happens sporadically, it's unusual for it to happen two months in a row and seems be a symptom of low inventory and climbing interest rates.

o

Inventory is trending up slightly compared to a

week ago for single family homes in all three counties with condos down

slightly in both Marin and San Francisco

o

But compared to a year ago numbers are down

across the board. San Francisco down

approx. 15%; Marin down 40% in single family homes and down 35% in condos.

·

Fundamentals:

o

San Francisco number of sales of single family

homes is down compared to January (22 vs 28) but overall number of sales was

higher in February than January, as expected.

o

San Francisco average selling prices are

generally up compared to the previous month, with 3/2 homes essentially flat.

However, compared to a year ago average selling prices for single family homes are

down 19% and average selling prices for condos is up slightly 2%.

o

San Francisco DOM is down substantially across

the board and premiums are up

o

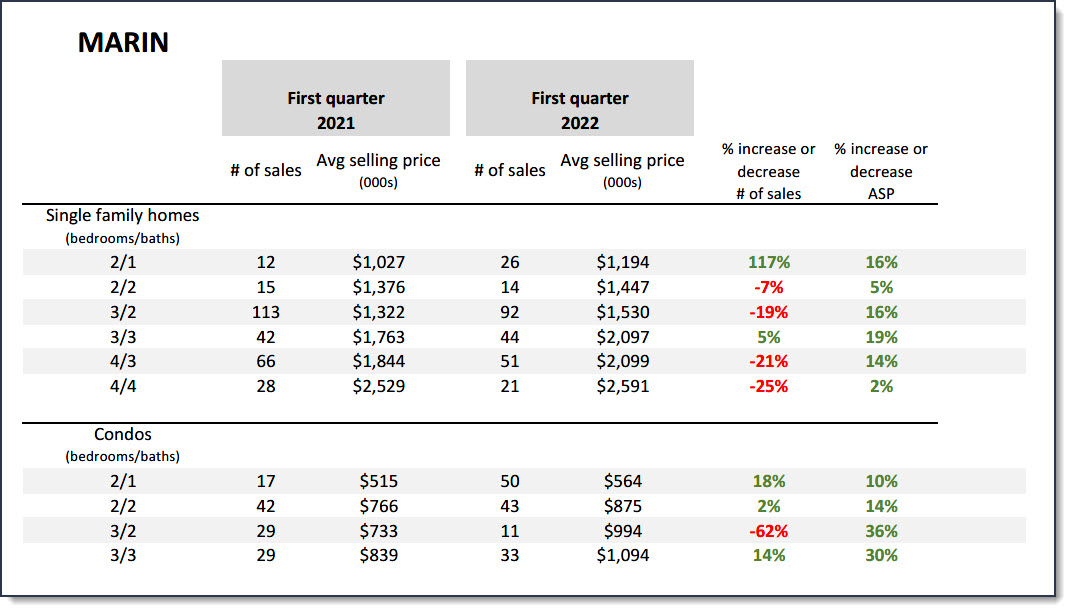

Marin number of sales of single family homes is

up, as expected.

o

Marin average selling prices are down slightly overall

for both single family homes and condos with the notable exception of 3/2, 3/3

and 4/4 configurations. Compared to a

year ago average selling prices for single family homes are down by 6% but

condos are up by almost 10%.

o

Marin DOM is down significantly overall and

premiums are up.

·

So, overall, month-to-month inventory numbers

are following typical trends for this time of year but, again, compared to a

year ago volume is down.